ABOUT ME

I’ve been a mortgage associate since 2007 and love what I do.

There are many types of mortgages, from residential to commercial. It is my job to find the most cost-effective mortgage for you and tailor it to your needs.

Being in the industry for as long as I have I have acquired extensive knowledge and experience and built a lot of relationships, all to serve you better.

Let me be your personal mortgage manager who you can call about your current or subsequent mortgages!

STEP ONE

Get Connected

STEP TWO

Evaluate Options

LENDERS

MORTGAGE ARTICLES

Let's run some numbers

Start by telling us where you're at in your home buying journey.

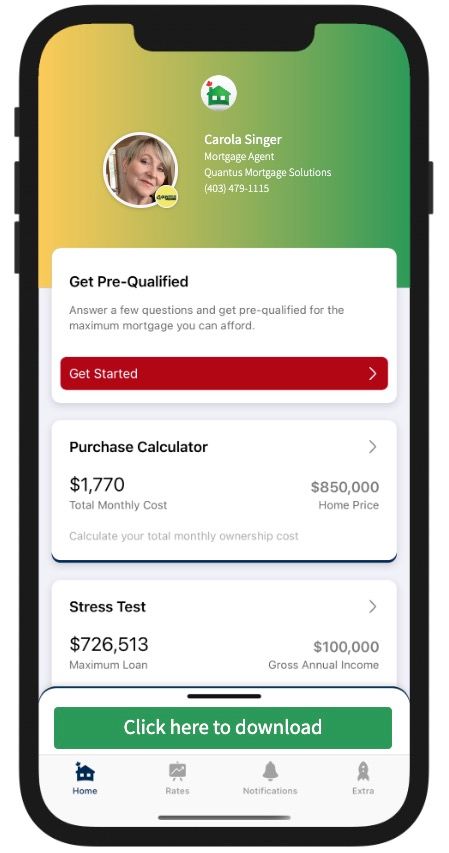

Download my App

What you can do with my app

Calculate your total cost of owning a home

Estimate the minimum down payment you need

Calculate Land transfer taxes and the available rebates

Calculate the maximum loan you can borrow

Stress test your mortgage

Estimate your Closing costs

Compare your options side by side

Search for the best mortgage rates

Email Summary reports (PDF)

Use my app in English, French, Spanish, Hindi, and Chinese